Most accounting systems include Value Added Tax (VAT) functions that can be customised to meet the requirements of GST.

If you want any guidance on the GST requirements for your accounting system, contact us.

You must keep a record of all business transactions that affect the amount of GST you have to pay, or can reclaim.

-

annual accounts, including trading and profit and loss accounts

-

bank statements and paying-in slips

- cash books and other account books

- credit or debit notes you issue or receive

- import and export documents

- orders and delivery notes

- purchase and sales books

The evidence you must keep includes:

-

purchase invoices and copy sales invoices

- records of daily takings such as till rolls

- relevant business correspondence

- your GST account

If you keep your records on a computer system it must be able to print out records and transactions at the request of our officers.

If your system has been provided by a third party, or is part of a computer system located outside of Jersey, you will need to be able to explain to our officers how the system operates when they visit your business. Make sure you have system and operating documents ready before the visit.

GST is usually charged on the supply of goods and services in Jersey, but can also be charged on the supply of certain services from outside Jersey. These include things like:

- advertising services

- consultants

- accountants

- financial services

- website hosting

- distance learning

For a full list, see Schedule 3 of the GST law.

Goods and Services Tax (Jersey) Law 2007 on Jersey Law website

When you import goods, you must keep evidence of Customs entry and duty payments and any other commercial documents related to the importation. This will help you prove any claim you make for a GST refund.

For more information on the importation process, see 'Pay GST when you import goods'.

Importing goods and paying GST

For GST purposes, goods and services that are exported are zero-rated.

You must keep evidence of Customs payments and any other commercial documents related to exporting goods. This will help you prove any claim you make for a GST refund.

If your business is registered for GST, you must issue a GST invoice whenever you supply taxable goods or services.

Make sure you keep all the GST invoices you receive when you buy taxable supplies for use in your business - you may be able to claim a GST refund when you submit your return.

GST taxed on goods and services

What a GST invoice must include

When you issue a GST invoice, it must show the following information:

- the words ‘tax invoice’ in a prominent place

- tax point date (the date on which the transaction took place)

- date of issue (if different from tax point date)

- your name, address and GST registration number

- name of the person you're supplying the goods to

- individual serial number

- description of the goods or services

- selling price

- amount of GST charged

- price including GST

- an indication as to whether GST is chargeable on the supply

- the amount of GST charged

The GST account is a simple summary within your accounting system (often part of the nominal ledger) which lists the following for each accounting period:

- the different sources of input tax and a total

- the different sources of output tax and a total

- any adjustments

- the net amount of GST payable

The figures above are used to complete your GST return.

You can adjust your GST invoices using credit and debit notes if all of the following conditions are met:

- a supply of goods or services is cancelled

-

the tax charged on a supply changes due to a variation in the supply

-

the agreed payment for the supply is altered

-

the goods or services supplied, or part of the supply is returned to the supplier

These conditions apply only where you have issued a GST invoice for the supply and the GST you charged was incorrect.

A credit note cannot be used to cancel a supply where the customer has not paid for it.

Credit note issued by a registered supplier

This reduces the supplier’s output tax and the recipient’s input tax for the period in which the credit note is issued.

Debit note issued by a registered supplier

This increases the supplier’s output tax and increases the recipient’s input tax for the period in which the debit note is issued.

Retailers can issue simplified GST invoices for retail sales up to a GST-inclusive value of £250. The information required on a simplified invoice is:

- name and address of supplier

- the supplier’s GST number

- date

- a brief description of the goods or services

- the gross amount charged

- the rate of GST applicable*

*Where the invoice includes items that are zero-rated for or exempt from GST, the value(s) of these will need to be identified.

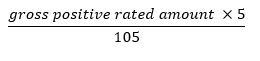

The supplier’s output tax is calculated by multiplying the gross positive rated amount (the total value of everything in the transaction liable to the standard rate of GST) by the 'GST fraction.

This amount of GST is also the customer’s input tax.

GST retail scheme

Self-billing is commonly used in commercial transactions where the value of the supply is not immediately known, such as sales of agricultural produce to a cooperative or wholesaler.

The receiver of goods or services can issue a sales invoice on behalf of the supplier.

If the supplier is registered for GST, the invoice must show the GST charged (once it is known) and the supplier’s GST registration number.

If the receiver is registered for GST, they can retain a copy of the self-billed invoice and claim input tax.

The GST amount is the supplier’s output tax.

You can only use self-billing if you have a written agreement between the receiver and the supplier which has been approved by the GST team.

You must keep your GST records for six years after the period they relate to. If you don't, you may face penalties.

If your records are lost or destroyed, write to us immediately, giving full details of how it happened. Our officers will advise you.

Once you are registered for GST, our officers will visit your business to examine your books and records. You can speed up these visits by making sure your records are complete and accurate.

Visits by GST officers to your business

gov.je

gov.je